The Global Economy in 2026 Navigates Amid New "Anchors"

Under the influence of tariff policies, geopolitical conflicts, and polarization among major powers, the global economy is projected to continue facing pressure in 2026. However, growth momentum will be offset by national investments in sovereignty and artificial intelligence (AI).

Under the influence of tariff policies, geopolitical conflicts, and polarization among major powers, the global economy is projected to continue facing pressure in 2026. However, growth momentum will be offset by national investments in sovereignty and artificial intelligence (AI).

2025 Momentum

In 2025, the global economy demonstrated greater resilience than expected, with growth improving compared to forecasts made at the beginning of the year. Nevertheless, significant disparities among economies and sectors persisted, and many structural risks remained.

According to the IMF, global growth in 2025 is estimated at 3.3%, on par with the previous year; while the World Bank estimates growth at 2.7%, 0.1 percentage points lower than the previous year. The U.S. continues to maintain positive growth, though the primary driver is no longer consumer spending but rather government spending and industrial-defense support packages. China continues to grow below its potential due to a slow recovery in the real estate market, weak consumer demand, and pressure from the international trade environment. The Eurozone faces prolonged low growth, simultaneously affected by high energy costs, weak domestic demand, industrial competition pressures, and tariff risks.

Global inflation in 2025 is projected to decline to 4.1%, lower than the 2022–2024 range (6.6%–8.7%) but still higher than pre-pandemic levels (1.9%–2.2%). Core inflation in many major economies remains above target levels, limiting and unevenly distributing room for monetary easing. International trade faces pressure from protectionist trends, supply chain restructuring, and high capital costs, while the “front-loading” effect gradually weakens.

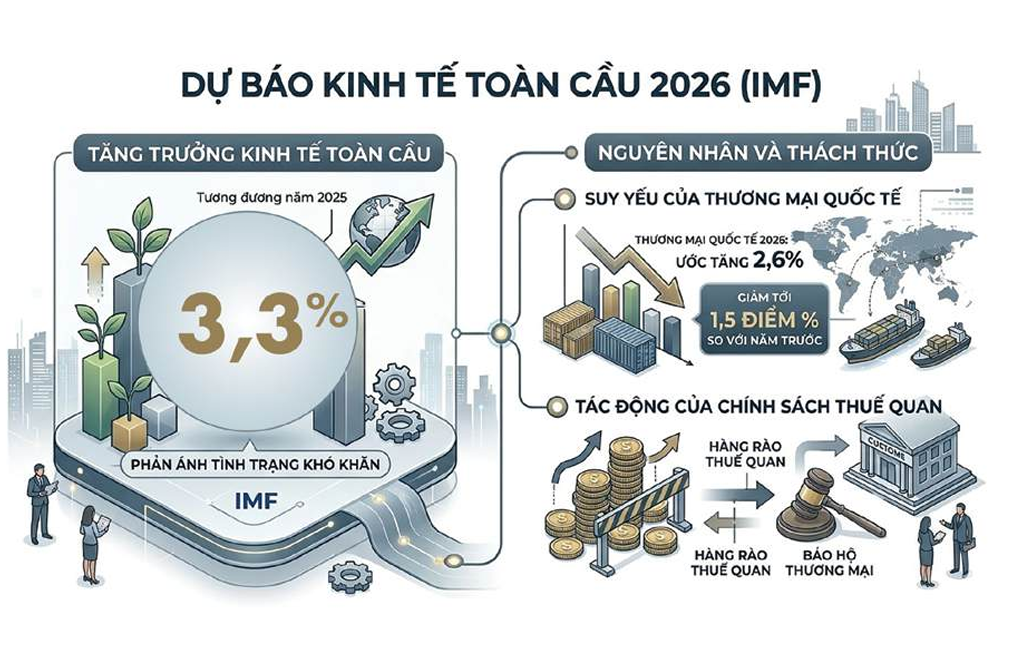

These developments are expected to continue into 2026. According to IMF projections, global economic growth in 2026 will reach 3.3% (on par with 2025), reflecting the challenges posed by the weakening of international trade (estimated to grow by 2.6%, a decrease of 1.5 percentage points from the previous year) and the impact of tariff policies. Although global inflation continues to ease (to around 3.8%), creating some room for a modest reduction in policy rates, major central banks are expected to maintain a cautious approach.

Of even greater concern is the highly unpredictable nature of the conflict in Iran specifically and the broader Middle East. Under the base-case scenario (50% probability), the conflict will last 4–5 years even if the conflict is limited to the U.S., Israel, and Iran. Meanwhile, under the negative scenario (30% probability), the conflict will spread across the Middle East and North Africa, leading to a prolonged blockade of the Strait of Hormuz. Under the very negative scenario (20% probability), tensions will escalate severely as major powers like Russia and China become involved. Regardless of the scenario, global economic growth will be significantly impacted. Typically, for every $10 increase in oil prices per barrel, global GDP decreases by 0.07–0.1 percentage points, and inflation rises. Meanwhile, Iran plays a pivotal role as the country with the world’s third-largest oil reserves. The Strait of Hormuz handles 20%–25% of global oil shipments. If the strait were completely blockaded, Brent crude prices could surpass the $100 per barrel mark, potentially reaching as high as $140 per barrel. According to forecasts by J.P. Morgan and Bank of America, gold prices would also be driven to “unprecedented” levels, potentially reaching $6,000–$6,300 per ounce by the end of 2026. Meanwhile, global financial markets will face severe turbulence.

Amid these risks, major economies are expected to “struggle” in their quest for growth. Edmond de Rothschild forecasts that the Eurozone economy will grow by only 0.8%, the U.S. by 1.9%, and China by 4.9%.

Despite higher growth rates, China’s economy is still viewed as unable to escape its downward trend, despite strong export growth driven by global demand for energy transition goods (such as solar panels, wind turbines…), AI infrastructure, and monetary policy support.

Meanwhile, European exports are expected to be heavily impacted by U.S. tariff hikes and the strengthening of the euro. Europe’s contribution to international trade is projected to remain negative in 2026. Ongoing uncertainty continues to dampen investment and consumption while encouraging savings, making economic growth in this region weak.

The anchors of the global economy in 2026

The polarization among nations and economies reflects the retreat of the globalization trend—a trend that began when Donald Trump was first elected U.S. president and was exacerbated by the COVID-19 pandemic. Escalating trade tensions in the post-pandemic years, linked to the tariff war, have further deepened this process. This has driven nations to intensify the implementation of sovereign policies, particularly in “critical” sectors, to reduce dependence, enhance resilience and adaptability to new shocks, and strengthen their own power.

A prime example is the United States, where the implementation of a “tit-for-tat” tariff policy is a key strategy to balance its trade position and rebuild industrial capacity, allowing the world’s wealthiest nation to consolidate its sovereignty. Although recently (in February 2026), tariffs under the International Emergency Economic Powers Act (IEEPA) were repealed following a ruling by the U.S. Supreme Court (SCOTUS), halting the retaliatory tariffs previously imposed by the Donald Trump administration, the White House immediately implemented a temporary 10% import surcharge based on Section 122 of the Trade Act of 1974. This tariff applies for a maximum of 150 days (i.e., until July 24, 2026) and may be extended if authorized by the U.S. Congress. In addition to tariffs, Washington is implementing a strategy to weaken the U.S. dollar by encouraging American households to hold more government bonds.

It is no coincidence that Edmond de Rothschild observes that today the global economy is no longer driven by globalization but by the sovereignty aspirations of major nations, through new investments and alliances. This is seen as a key driver of global growth in 2026, and even in the years to come.

In fact, the implementation of sovereignty policies (in sectors such as industry, energy, food, digital technology, and media) is currently the most prominent trend in the global economy. Edmond de Rothschild estimates that investments in sovereignty amount to 5.3% of global GDP, or approximately $6 trillion.

Among these, military spending is growing at the fastest rate. From 2022 to 2024, global military spending increased by 9% annually in nominal USD terms, far outpacing the 2.4% growth rate observed between 2010 and 2021. In 2024, global military spending recorded its strongest increase since the end of the Cold War, rising by 11% in nominal USD terms compared to 2023, reaching $2.718 trillion, equivalent to 2.5% of global GDP. European nations have significantly increased military spending, particularly Germany, Poland, the Netherlands, Finland, and the Czech Republic.

In addition to sovereignty policies, investment in AI has also been robust, providing strong support for global growth. It is estimated that between 2022 and 2025, spending on AI-related infrastructure has increased by $400 billion. According to Manuel Maleki, Deputy Director and U.S. Economist at Edmond de Rothschild, the multiplier effect of AI investment could boost GDP by 0.3%–0.5% annually.

In summary, it is evident that global growth in 2026 will face pressure from a decline in international trade due to tariffs and geopolitical conflicts. However, these negative impacts will be offset by investments in sovereignty and artificial intelligence.

As the world shifts from polarization to fragmentation, highly open economies (including Vietnam) will face significant challenges, requiring flexible policies to adapt, seek opportunities for growth while maintaining autonomy, especially as major economies use growth as a tool of power.

Le Hai