The New Landscape of Vietnam’s Stock Market

On April 8, 2026, FTSE Russell officially confirmed the upgrade of the Vietnamese stock market from Frontier Market to Secondary Emerging Market, following the completion of its mid-year review. This is a significant milestone, marking a highly positive step forward and providing strong momentum for the development of the Vietnamese stock market during the 2026–2030 period. Based on lessons learned from countries that have been upgraded in the past, the Vietnamese stock market is expected to benefit from these positive developments.

On April 8, 2026, FTSE Russell officially confirmed the upgrade of the Vietnamese stock market from Frontier to Secondary Emerging, following the completion of the mid-term review. This is a significant milestone, marking a highly positive step forward and providing strong momentum for the development of the Vietnamese stock market during the 2026–2030 period. Based on lessons learned from countries that have been upgraded in the past, the Vietnamese stock market is expected to benefit from positive developments and numerous new opportunities.

Surge in foreign capital inflows and improved market liquidity

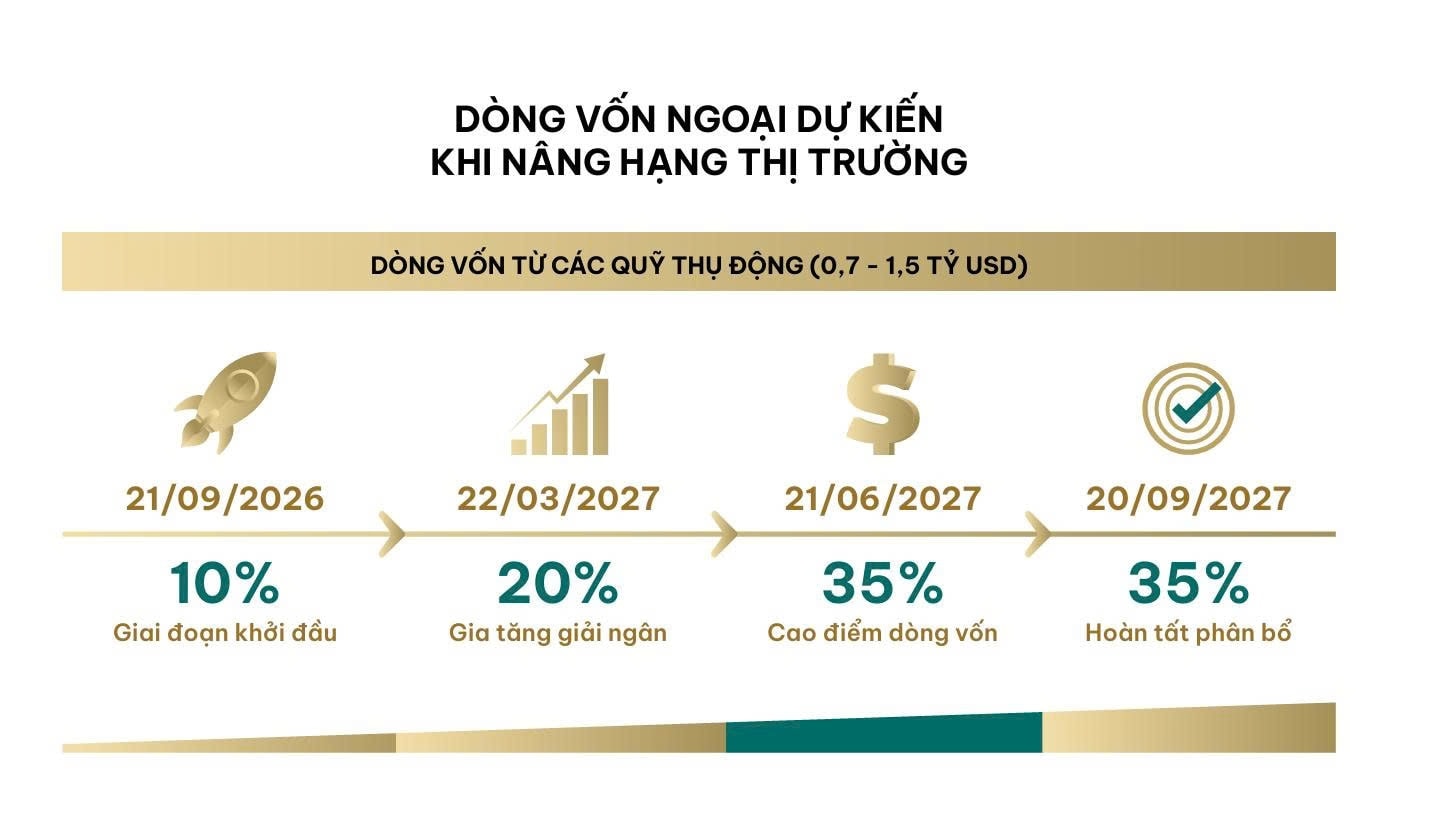

Capital inflows from passive funds are projected to bring in 0.7–1.5 billion USD, allocated across four phases with specific timelines and weightings as follows: Phase 1 (September 21, 2026): 10%; Phase 2 (March 22, 2027): 20%; Phase 3 (June 21, 2027): 35%; and Phase 4 (September 20, 2027): 35%.

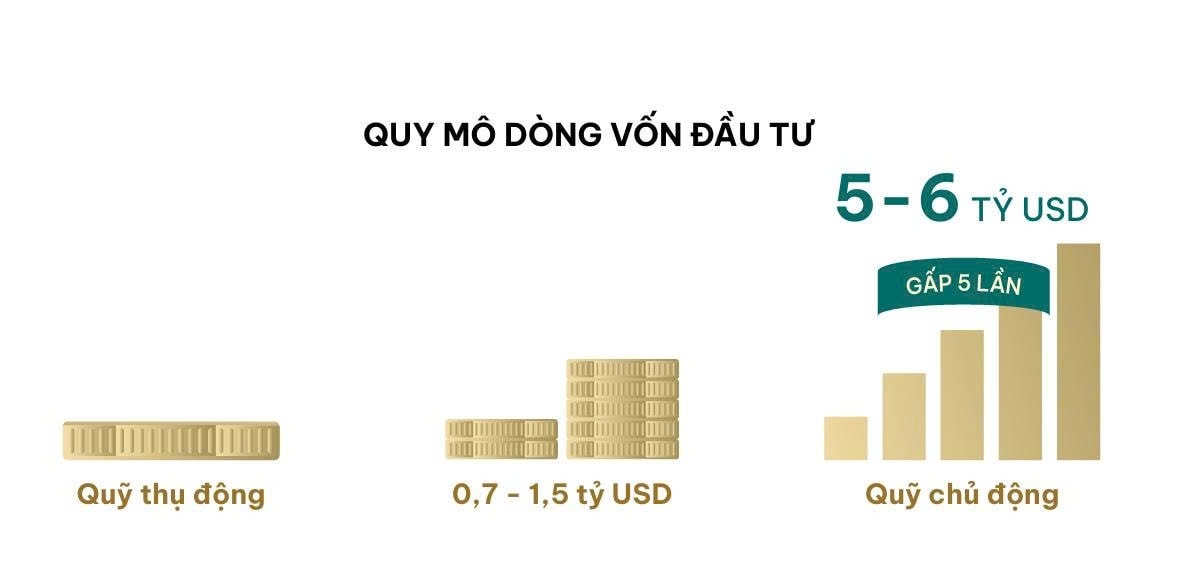

Additionally, according to experts from FTSE, the scale of active funds is expected to be five times larger than that of passive funds, bringing in approximately $5–6 billion in foreign indirect investment capital.

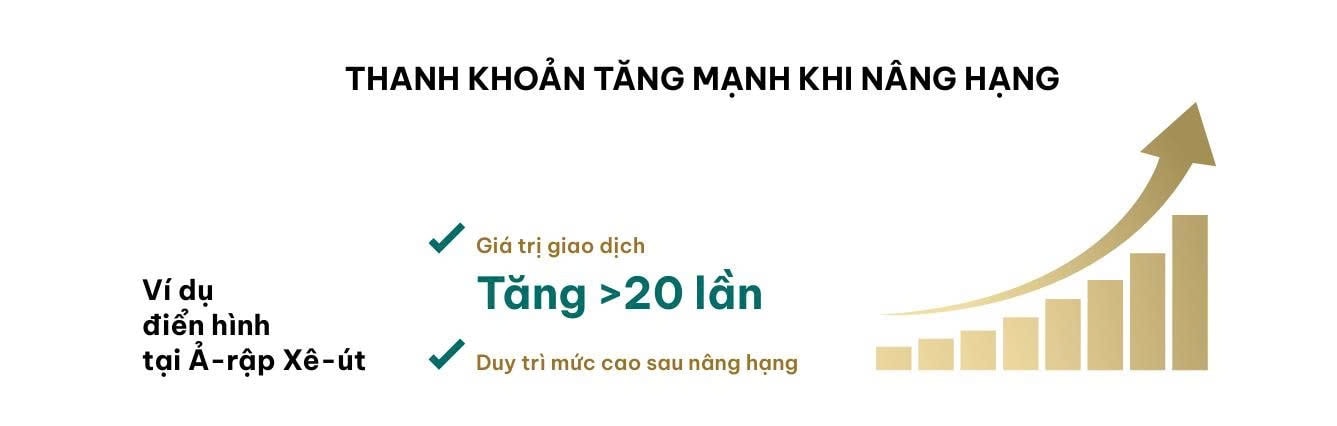

On the other hand, the upgrade will fundamentally increase market liquidity—a prime example being Saudi Arabia, which saw trading volumes increase more than 20-fold immediately prior to the upgrade and remain at high levels thereafter.

1. Infrastructure Development and New Products

The upgrade process is accompanied by the implementation of advanced products and systems, including: green securities/bonds, new derivatives, securities lending and borrowing, controlled short selling, day trading… and notably, the Central Counterparty (CCP) system.

2. A “springboard” for the IPO and divestment wave

Opportunities to accelerate IPOs, market transfers (from UPCoM to HOSE/HNX), as well as the privatization and divestment of State-owned enterprises to leverage large capital inflows from international sources.

3. Improving corporate governance

The upgrade process requires domestic companies to raise internal governance standards, adopt ESG evaluation systems in line with international best practices, and gradually transition to International Financial Reporting Standards (IFRS).

4. Promoting policy commitments and institutional reforms

Upgrading creates a "ripple effect on regulatory agencies’ policy commitments." This process compels agencies to continuously refine the legal framework for sustainable development in line with international best practices, such as addressing foreign ownership limits (foreign ownership caps).

5. Restructuring the investor base

This development creates a favorable foundation for attracting the participation of institutional investors and international financial institutions. Lessons from Saudi Arabia show that, following the upgrade, the ownership ratio of institutional investors in that market surged from 68% to 91%, helping to make the market structure more robust and professional while reducing reliance on speculative capital flows from individual investors.

6. Spillover Effects on Foreign Direct Investment (FDI)

The benefits of an upgrade extend beyond the stock market to positively impact the real economy. Upgrades have been shown to significantly boost FDI inflows; for example, FDI in India increased by 49% and in Egypt by 63% within just one year after being included in the MSCI index.

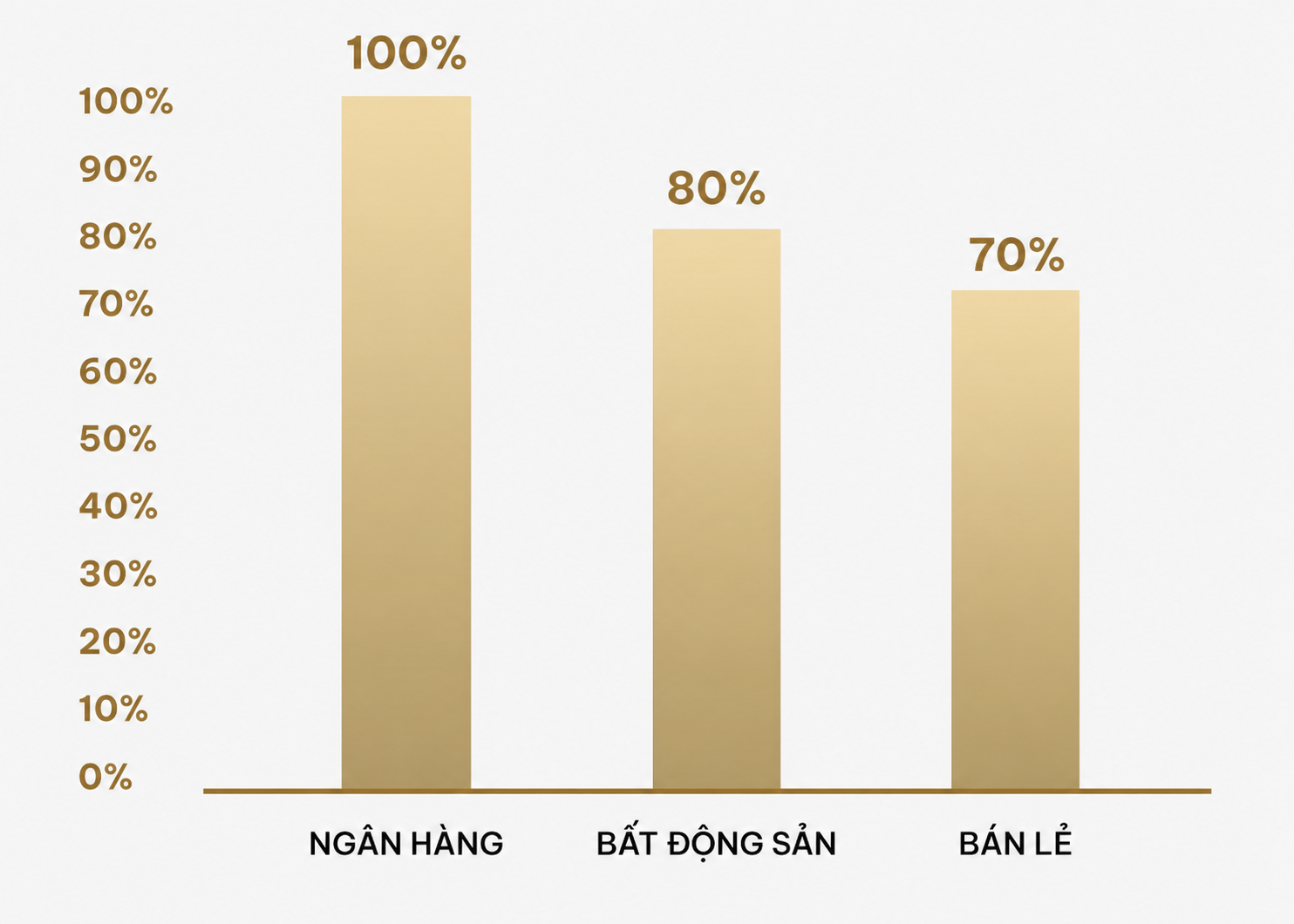

1. The banking sector

Efforts to achieve the 10% GDP growth target for the 2026–2030 period are expected to attract active capital from investment funds following the upgrade (market consensus estimates up to 4–5 billion USD), alongside approximately 1 billion USD in passive ETF inflows.

The banking sector will benefit in terms of profit growth (linked to economic growth) and in terms of cash flow (accounting for >40% of the VN-Index market capitalization).

Regarding the 2026 outlook, system-wide credit growth is expected to reach 17% (higher than the 15% target set at the beginning of the year). Fundraising will continue to face challenges; active efforts to attract foreign capital are expected to support liquidity. CSTK plays a central role in providing seed capital.

2. Real Estate Sector

Expanding capital mobilization channels: An upgrade is expected to attract approximately $5–6 billion in foreign capital, of which ~$1 billion will come from ETFs and the remainder from active funds. This creates opportunities for real estate companies to diversify their funding sources while enhancing access to international investors and partners.

Outlook remains dependent on internal factors: The upgrade does not alter the core factors driving the sector, including credit policies, interest rates, and the legal environment. Corporate performance still depends primarily on project quality, location, and implementation capabilities.

3. Retail Sector

Capital inflows and foreign ownership limits: Leading stocks (MSN, VNM, FRT...) continue to attract foreign capital to expand their scale and improve management capabilities. Monitor technical solutions (ETFs, depositary receipts) for companies that have reached their foreign ownership limit (MWG, PNJ, etc.).

2026 – Marking a new growth cycle: Net profit for 2026 is expected to grow by >+15% YoY (accounting for ~6% of the market’s total net profit) driven by operational optimization and a significant shift from traditional channels to modern channels (Modern Trade) by leading companies, under regulatory frameworks promoting transparency.