The third wave of IPOs on the Vietnamese stock market

The third wave of IPOs is forming on the Vietnamese stock market, amid improved liquidity and expectations of a market upgrade.

Many large-scale enterprises are preparing to go public, promising to open up a new cycle of opportunities for investors.

1. The state of IPOs in Vietnam from 2005 to 2025

From 2000 to 2024, the Vietnamese stock market recorded two IPO waves occurring during the periods (2007-2009) and (2017-2018), with strong and primarily private sector participation. State-owned enterprises also actively participated during these periods; however, since 2019, state-owned enterprises have been largely absent from IPO activities.

With the comprehensive reform efforts of the regulatory agency to upgrade the Vietnamese stock market, combined with FTSE Russell's announcement of approval for an upgrade in October 2025, the third wave of IPOs is beginning to show optimistic signs – expectations for a new beginning with many attractive IPO deals in the 2025-2027 period.

IPO/listing activities are also taking place among FDI enterprises, though the number recorded is insignificant. After the Government issued Decree 38/2003/ND-CP on April 15, 2003, and the National Assembly passed the Investment Law in 2005 (replacing the Law on Foreign Investment and the Law on Domestic Investment), the stock market recorded an IPO/listing trend among FDI enterprises in the market's first wave of IPOs. Specifically, 2006-2010 saw 10 enterprises listed, but this trend declined sharply and by 2025, the market recorded only one enterprise listed on the HoSE in 2017.

2. IPO activities, capital increases, auctions, listings, and securities registration on the Vietnamese stock market in 2025

The total value of (1) IPOs, (2) capital increases (private placements + stock options), and (3) successful auctions in 2025 reached over VND 148 trillion.

Of which: (i) IPO activities at 03 securities companies attracted 35,672 billion VND; (ii) capital increase activities reached VND 106,399 billion; and (iii) auction activities reached VND 6,725 billion – with two major deals at Vietnam Electronics and Information Technology Corporation (VITAC) (VND 2,562 billion) and Vietnam Water and Environment Investment Corporation (VWI) (VND 1,231 billion).

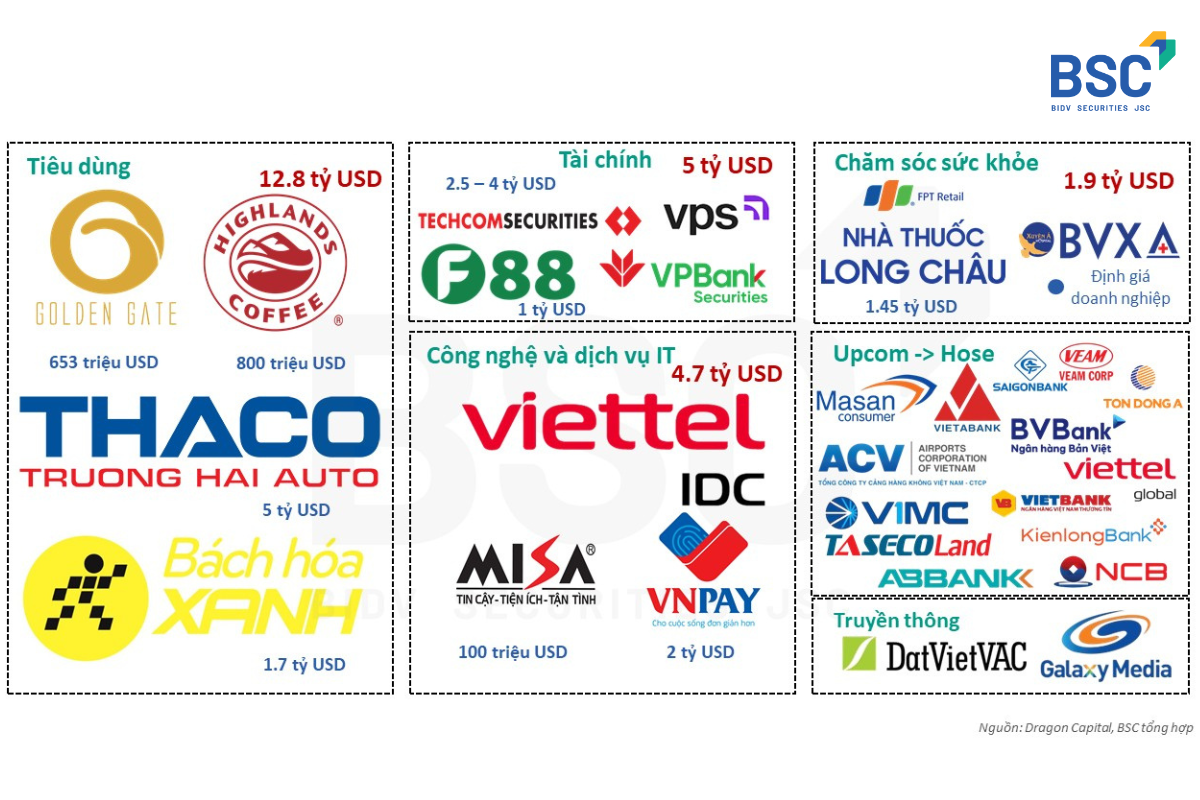

It is expected that IPO activities will continue to be vibrant in the coming period, with capital increase plans – the planned value is expected to reach nearly VND 100 trillion. This may affect market liquidity as a portion of funds has been and will be attracted amid the strong resurgence of IPOs/capital increases/auctions.

3. The "liquidity-draining effect" following large-scale capital raising rounds on the market

Market liquidity tends to decline between capital raising rounds. Specifically, in months with large capital raising values, liquidity often increases but then declines afterward, indicating the "liquidity-sucking effect" appearing in the market.

A portion of the cash flow is withdrawn from the market to participate in large transactions (IPOs/private placements/exercising stock options for existing shareholders), which weakens the upward momentum and accelerates the market's adjustment process after the previous positive phase.

4. Investment performance when participating in IPO transactions in Vietnam

Expectations for returns from IPO stocks depend heavily on the timing of participation. Before deciding to participate in IPO deals, investors need to determine the time frame: short-term and long-term.

Short-term (less than 3 months): investment performance will depend on cash flow and timing. The main drivers of price increases are media hype and temporary supply shortages. Based on historical data from booming years such as 2021 or 2024, the win rate can reach up to 50%. However, the risk is also present: when market liquidity tightens, the probability of profit decreases significantly. Therefore, in the short term, timing is more important.

Long-term (1-3 years): investment performance shows a clear divergence. For example, in 2012: after 3 years, the median return on IPO stocks was -28.9%, but the average return reached +47.4%. This proves that even when the market is struggling, truly high-quality stocks will still achieve superior growth. Therefore, the factor of company selection will replace the general trend.

For detailed insights, refer to the report "Market Waves: The Third IPO Wave and the History of Capital Raising on the Vietnamese Stock Market": Here

Source: BIDV Securities (BSC)